Example I: Multiple linear regression

Let us start with a linear regression example. First, load the packages needed:

using ProfileLikelihood

using Random

using PreallocationTools

using Distributions

using CairoMakie

using LinearAlgebra

using Optimization

using OptimizationOptimJL

using Test

using StableRNGsWe perform a simulation study where we try and estimate the parameters in a regression of the form

\[y_i = \beta_0 + \beta_1x_{1i} + \beta_2x_{2i} + \beta_3x_{1i}x_{3i} + \varepsilon_i, \quad \varepsilon_i \sim \mathcal N(0, \sigma^2), \quad i=1,2,\ldots, n. \]

We also try and estimate $\sigma$.

Setting up the problem

Let us start by simulating the data:

using Random, Distributions, StableRNGs

rng = StableRNG(98871)

n = 600

β = [-1.0, 1.0, 0.5, 3.0]

σ = 0.05

x₁ = rand(rng, Uniform(-1, 1), n)

x₂ = rand(rng, Normal(1.0, 0.5), n)

X = hcat(ones(n), x₁, x₂, x₁ .* x₂)

ε = rand(rng, Normal(0.0, σ), n)

y = X * β + εThe data y is now our noisy data. The likelihood function in this example is

\[\ell(\sigma, \boldsymbol \beta \mid \boldsymbol y) = -(n/2)\log(2\mathrm{\pi}\sigma^2) - (1/2\sigma^2)\sum_i (y_i - \beta_0 - \beta_1x_{1i} - \beta_2x_{2i} - \beta_3x_{1i}x_{2i})^2. \]

We now define our likelihood function. To allow for automatic differentiation, we use PreallocationTools.DiffCache to define our cache vectors.

sse = DiffCache(zeros(n))

β_cache = DiffCache(similar(β), 10)

dat = (y, X, sse, n, β_cache)

@inline function loglik_fnc(θ, data)

σ, β₀, β₁, β₂, β₃ = θ

y, X, sse, n, β = data

_sse = get_tmp(sse, θ)

_β = get_tmp(β, θ)

_β[1] = β₀

_β[2] = β₁

_β[3] = β₂

_β[4] = β₃

ℓℓ = -0.5n * log(2π * σ^2)

mul!(_sse, X, _β)

for i in eachindex(y)

ℓℓ = ℓℓ - 0.5 / σ^2 * (y[i] - _sse[i])^2

end

return ℓℓ

endNow having defined our likelihood, we can define the likelihood problem. We let the problem be unconstrained, except for $\sigma > 0$. We start at the value $1$ for each parameter. To use automatic differentiation, we use Optimization.AutoForwardDiff for the adtype.

using Optimization

θ₀ = ones(5)

prob = LikelihoodProblem(loglik_fnc, θ₀;

data=dat,

f_kwargs=(adtype=Optimization.AutoForwardDiff(),),

prob_kwargs=(

lb=[0.0, -Inf, -Inf, -Inf, -Inf],

ub=Inf * ones(5)

),

syms=[:σ, :β₀, :β₁, :β₂, :β₃]

)

LikelihoodProblem. In-place: true

θ₀: 5-element Vector{Float64}

σ: 1.0

β₀: 1.0

β₁: 1.0

β₂: 1.0

β₃: 1.0Finding the MLEs

Now we can compute the MLEs.

using OptimizationOptimJL

sol = mle(prob, Optim.LBFGS())

LikelihoodSolution. retcode: Success

Maximum likelihood: 953.0592307643246

Maximum likelihood estimates: 5-element Vector{Float64}

σ: 0.04942145761216433

β₀: -1.003655020311133

β₁: 0.9980076846106273

β₂: 0.5030706527702703

β₃: 2.9989096752667272We can compare these MLEs to the true MLES $\hat{\beta} = (\boldsymbol X^{\mathsf T}\boldsymbol X)^{-1}\boldsymbol X^{\mathsf T}\boldsymbol y$ and $\hat\sigma^2 = (1/n_d)(\boldsymbol y - \boldsymbol X\boldsymbol \beta)^{\mathsf T}(\boldsymbol y - \boldsymbol X\boldsymbol \beta)$, where $n_d$ is the degrees of freedom, as follows (note the indexing):

using Test, LinearAlgebra

df = n - (length(β) + 1)

resids = y .- X * sol[2:5]

@test sol[2:5] ≈ inv(X' * X) * X' * y # sol[i] = sol.mle[i]

@test sol[:σ]^2 ≈ 1 / df * sum(resids .^ 2) atol = 1e-4 # symbol indexingProfiling

We can now profile the results. In this case, since the problem has no bounds for some parameters we need to manually define the parameter bounds used for profiling. The function construct_profile_ranges is used for this. Note that we use parallel = true below to allow for multithreading, allowing multiple parameters to be profiled at the same time.

lb = [1e-12, -5.0, -5.0, -5.0, -5.0]

ub = [15.0, 15.0, 15.0, 15.0, 15.0]

resolutions = [600, 200, 200, 200, 200] # use many points for σ

param_ranges = construct_profile_ranges(sol, lb, ub, resolutions)

prof = profile(prob, sol; param_ranges, parallel=true)

ProfileLikelihoodSolution. MLE retcode: Success

Confidence intervals:

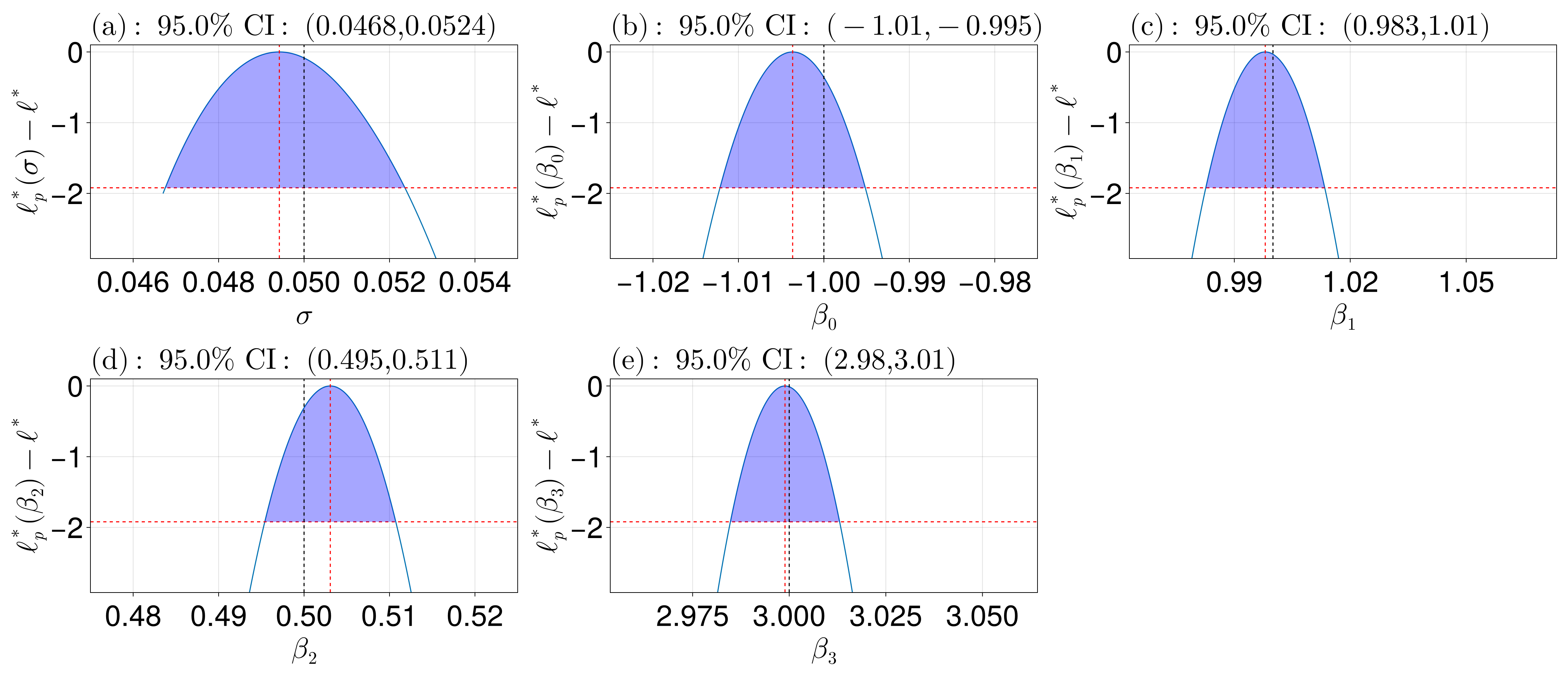

95.0% CI for σ: (0.04675191495089245, 0.052360551143196946)

95.0% CI for β₀: (-1.0121607844224445, -0.9951520336370397)

95.0% CI for β₁: (0.9826173262148143, 1.0133977395553302)

95.0% CI for β₂: (0.4954041345031461, 0.5107344459064201)

95.0% CI for β₃: (2.9847775716187175, 3.013042187605372)These confidence intervals can be compared to the true confidence intervals as follows, noting that the variance-covariance matrix for the $\beta_i$ coefficients is $\boldsymbol\Sigma = \sigma^2(\boldsymbol X^{\mathsf T}\boldsymbol X)^{-1}$ so that their confidence interval is $\hat\beta_i \pm 1.96\sqrt{\boldsymbol\Sigma_{ii}}$. Additionally, a confidence interval for $\sigma$ is $\sqrt{(\boldsymbol y - \boldsymbol X\boldsymbol \beta)^{\mathsf T}(\boldsymbol y - \boldsymbol X\boldsymbol \beta)}(1/\sqrt{\chi_{0.975, n_d}}, 1/\sqrt{\chi_{0.025, n_d}})$.

vcov_mat = sol[:σ]^2 * inv(X' * X)

for i in 1:4

@test prof.confidence_intervals[i+1][1] ≈ sol.mle[i+1] - 1.96sqrt(vcov_mat[i, i]) atol = 1e-3

@test prof.confidence_intervals[i+1][2] ≈ sol.mle[i+1] + 1.96sqrt(vcov_mat[i, i]) atol = 1e-3

end

rss = sum(resids .^ 2)

χ²_up = quantile(Chisq(df), 0.975)

χ²_lo = quantile(Chisq(df), 0.025)

σ_CI_exact = sqrt.(rss ./ (χ²_up, χ²_lo))

@test get_confidence_intervals(prof, :σ).lower ≈ σ_CI_exact[1] atol = 1e-3

@test ProfileLikelihood.get_upper(get_confidence_intervals(prof, :σ)) ≈ σ_CI_exact[2] atol = 1e-3You can use prof to view a single parameter's results, e.g.

julia> prof[:β₂] # This is a ProfileLikelihoodSolutionView

Profile likelihood for parameter β₂. MLE retcode: Success

MLE: 0.5030706527702703

95.0% CI for β₂: (0.4954041345031461, 0.5107344459064201)You can also evaluate the profile at a point inside its confidence interval. (If you want to evaluate outside the confidence interval, you need to use a non-Throw extrap in the profile function's keyword argument [see also Interpolations.jl].) The following are all the same, evaluating the profile for $\beta_2$ at $\beta_2=0.5$:

prof[:β₂](0.50)

prof(0.50, :β₂)

prof(0.50, 4)Visualisation

We can now also visualise the results. In the plot below, the red line is at the threshold for the confidence region, so that the parameters between these values define the confidence interval. The red lines are at the MLEs, and the black lines are at the true values.

using CairoMakie

fig = plot_profiles(prof;

latex_names=[L"\sigma", L"\beta_0", L"\beta_1", L"\beta_2", L"\beta_3"], # default names would be of the form θᵢ

show_mles=true,

shade_ci=true,

true_vals=[σ, β...],

fig_kwargs=(fontsize=41,),

axis_kwargs=(width=600, height=300))

xlims!(fig.content[1], 0.045, 0.055) # fix the ranges

xlims!(fig.content[2], -1.025, -0.975)

xlims!(fig.content[4], 0.475, 0.525)

resize_to_layout!(fig)

You could also plot individual or specific parameters:

plot_profiles(prof, [1, 3]) # plot σ and β₁

plot_profiles(prof, [:σ, :β₁, :β₃]) # can use symbols

plot_profiles(prof, 1) # can just provide an integer

plot_profiles(prof, :β₂) # symbols work